But the ultimate problem isn't the missing data but the premise. If monetary policy is effective, we shouldn't see much of a correlation between interest rates and housing starts because, by the nature of the Fed, interest rates should be low during recessions. That's one of the jobs of the Federal Reserve: keep unemployment low.

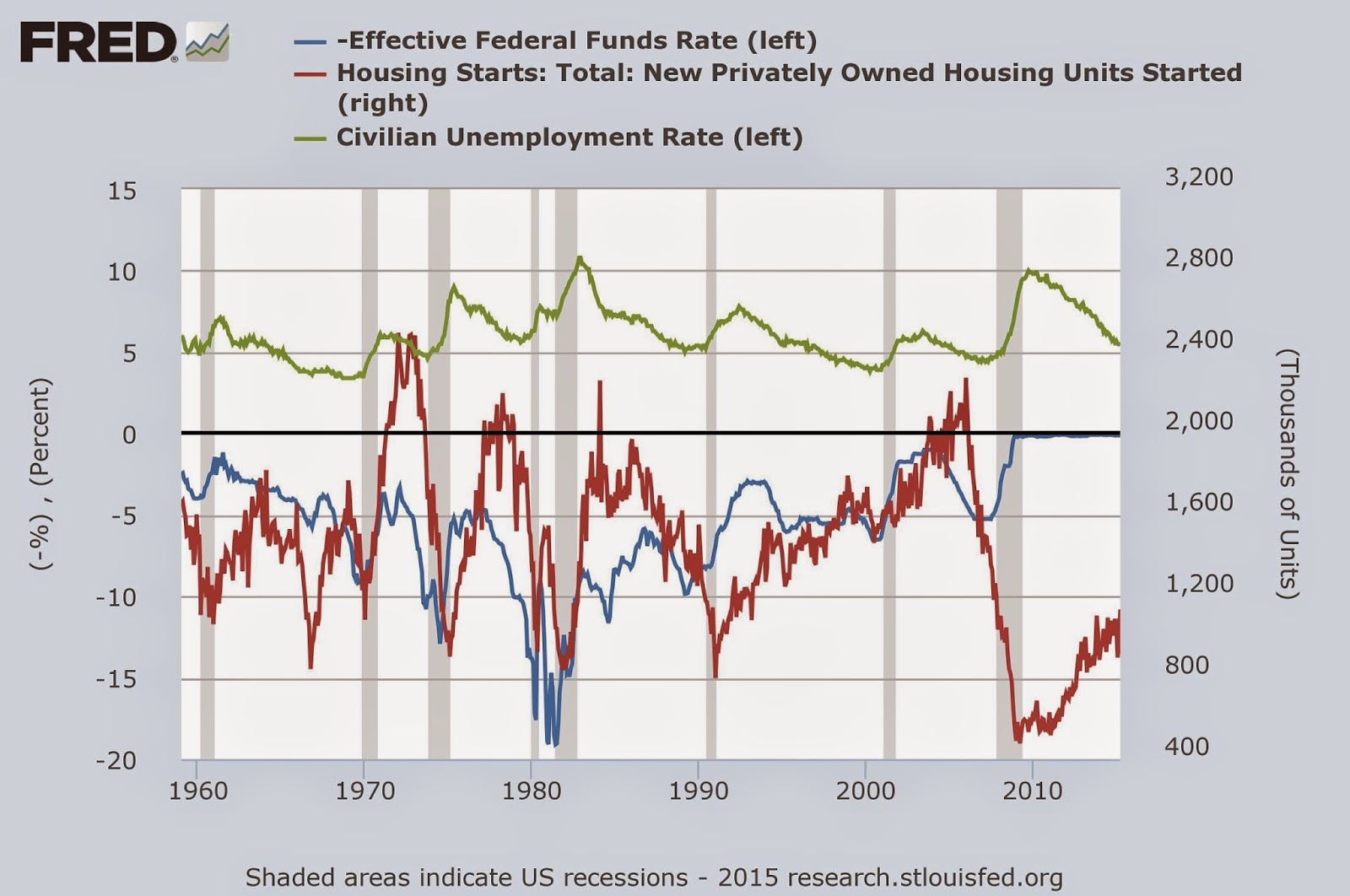

There's any number of appropriate variables you can pick to factor in market conditions but let's look at the big one: civilian unemployment. Here's the graph with civilian unemployment thrown in:

Unfortunately, it's hard to tell much from this but a regression can help. With change in interest rates AND unemployment predicting housing starts, we get:

- Unemployment

- Coefficient: -100.6

- T-Stat: -11.48 (statistically significant)

- Interest rate

- Coefficient: -22.7

- T-Stat: -5.91 (also statistically significant)

- R-squared: 0.202 (now we're explaining over 20% of the variation!)

I didn't remove that transformation when I ran the regression. Thus the negative coefficient means positive correlation between interest rates and housing starts. So despite the incomplete approach by his critics, Krugman still appears to be wrong.

But don't throw out the demand curve just yet. New housing starts don't just respond to monetary policy; monetary policy responds to new housing starts. It is the classic causation problem that comes up in statistical analysis, especially regressions.

This is why theory is so important; it just makes too much sense that as interest rates fall, people will want to borrow more. Untangling all the effects to demonstrate that is indeed the case--and to what degree that's the case--cannot be done with something as simple as a correlation coefficient.

1 comment:

Glad you are back. I still don't understand you.

Post a Comment