Boston gave up on its bid to host the 2024 Olympics on Monday, a surprisingly wise move given the city was home to the most expensive highway project in the US: the way over budget Big Dig. Maybe the whole ordeal made Bostonians suspicious of megaprojects. And rightfully so.

Projects that cost a billion dollars or more--whether private or public--tend to take much longer and cost much more than initially estimated. It's not simply corruption. It's also just very hard to estimate these parameters.

Olympic preparation is a particular dumb megaproject. The building big, special-use stadiums is outrageously expensive. And that doesn't include the upgrades to transportation infrastructure, hotel space, and other projects. Brazil faced protests in 2014 over its spending and forced relocation efforts for hosting the World Cup and Rio's experiencing some of those same protests again over its Olympic hosting. It's no wonder economists agree that hosting the Olympics is a bad deal.

Maybe having a new host city every four years made sense in 1896, when the modern Olympics first began. There was no television. Radio was only invented the year before. But in the Information Age, a rotating host city is an anachronism.

Keeping the Olympics in Athens eliminates many of these cost problems. Yes, the infrastructure would have to be maintained but it will be far less costly than recreating it every four years. Countries would loss the ability to gain prestige from hosting the Olympics, but hopefully more cities will realize it's a bad deal and that prestige will morph into embarrassment.

Wednesday, July 29, 2015

Saturday, July 04, 2015

Friday, May 22, 2015

On Foolish Correlations

James Montier and Paul Krugman are in a bit of a spat over how much interest rates matter. Krugman put forth data from FRED (Federal Reserve Economic Data) showing a strong correlation between interest rates and housing starts. But, says Cullen Roche, he left out 40% of the data, putting his whole thesis into question. A simple regression of the all the data yields an R-squared of just 0.0453 (in other words, interest rates predict about 4.53% of the variation in housing starts).

But the ultimate problem isn't the missing data but the premise. If monetary policy is effective, we shouldn't see much of a correlation between interest rates and housing starts because, by the nature of the Fed, interest rates should be low during recessions. That's one of the jobs of the Federal Reserve: keep unemployment low.

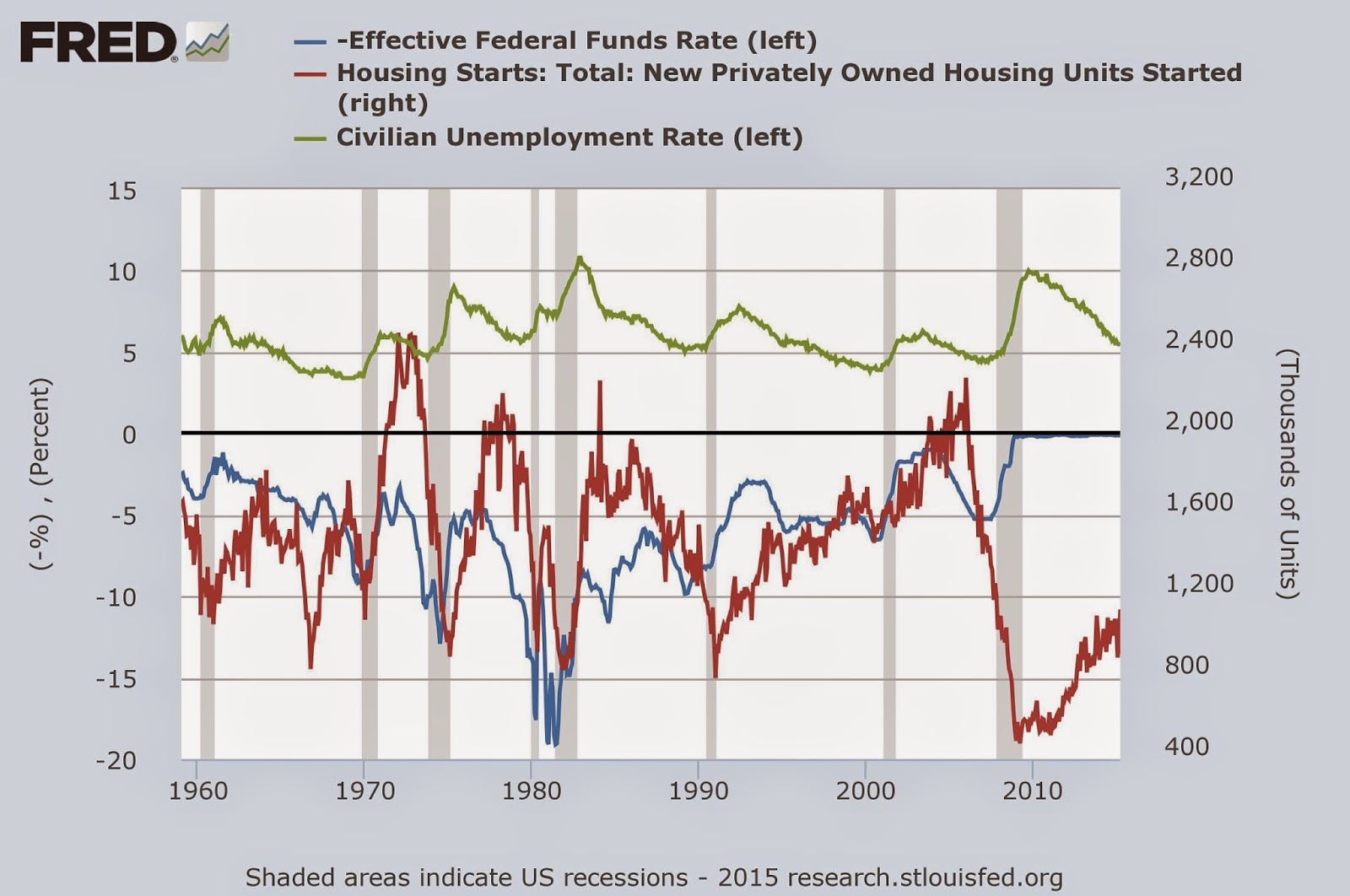

There's any number of appropriate variables you can pick to factor in market conditions but let's look at the big one: civilian unemployment. Here's the graph with civilian unemployment thrown in:

Unfortunately, it's hard to tell much from this but a regression can help. With change in interest rates AND unemployment predicting housing starts, we get:

I didn't remove that transformation when I ran the regression. Thus the negative coefficient means positive correlation between interest rates and housing starts. So despite the incomplete approach by his critics, Krugman still appears to be wrong.

But don't throw out the demand curve just yet. New housing starts don't just respond to monetary policy; monetary policy responds to new housing starts. It is the classic causation problem that comes up in statistical analysis, especially regressions.

This is why theory is so important; it just makes too much sense that as interest rates fall, people will want to borrow more. Untangling all the effects to demonstrate that is indeed the case--and to what degree that's the case--cannot be done with something as simple as a correlation coefficient.

But the ultimate problem isn't the missing data but the premise. If monetary policy is effective, we shouldn't see much of a correlation between interest rates and housing starts because, by the nature of the Fed, interest rates should be low during recessions. That's one of the jobs of the Federal Reserve: keep unemployment low.

There's any number of appropriate variables you can pick to factor in market conditions but let's look at the big one: civilian unemployment. Here's the graph with civilian unemployment thrown in:

Unfortunately, it's hard to tell much from this but a regression can help. With change in interest rates AND unemployment predicting housing starts, we get:

- Unemployment

- Coefficient: -100.6

- T-Stat: -11.48 (statistically significant)

- Interest rate

- Coefficient: -22.7

- T-Stat: -5.91 (also statistically significant)

- R-squared: 0.202 (now we're explaining over 20% of the variation!)

I didn't remove that transformation when I ran the regression. Thus the negative coefficient means positive correlation between interest rates and housing starts. So despite the incomplete approach by his critics, Krugman still appears to be wrong.

But don't throw out the demand curve just yet. New housing starts don't just respond to monetary policy; monetary policy responds to new housing starts. It is the classic causation problem that comes up in statistical analysis, especially regressions.

This is why theory is so important; it just makes too much sense that as interest rates fall, people will want to borrow more. Untangling all the effects to demonstrate that is indeed the case--and to what degree that's the case--cannot be done with something as simple as a correlation coefficient.

Subscribe to:

Posts (Atom)