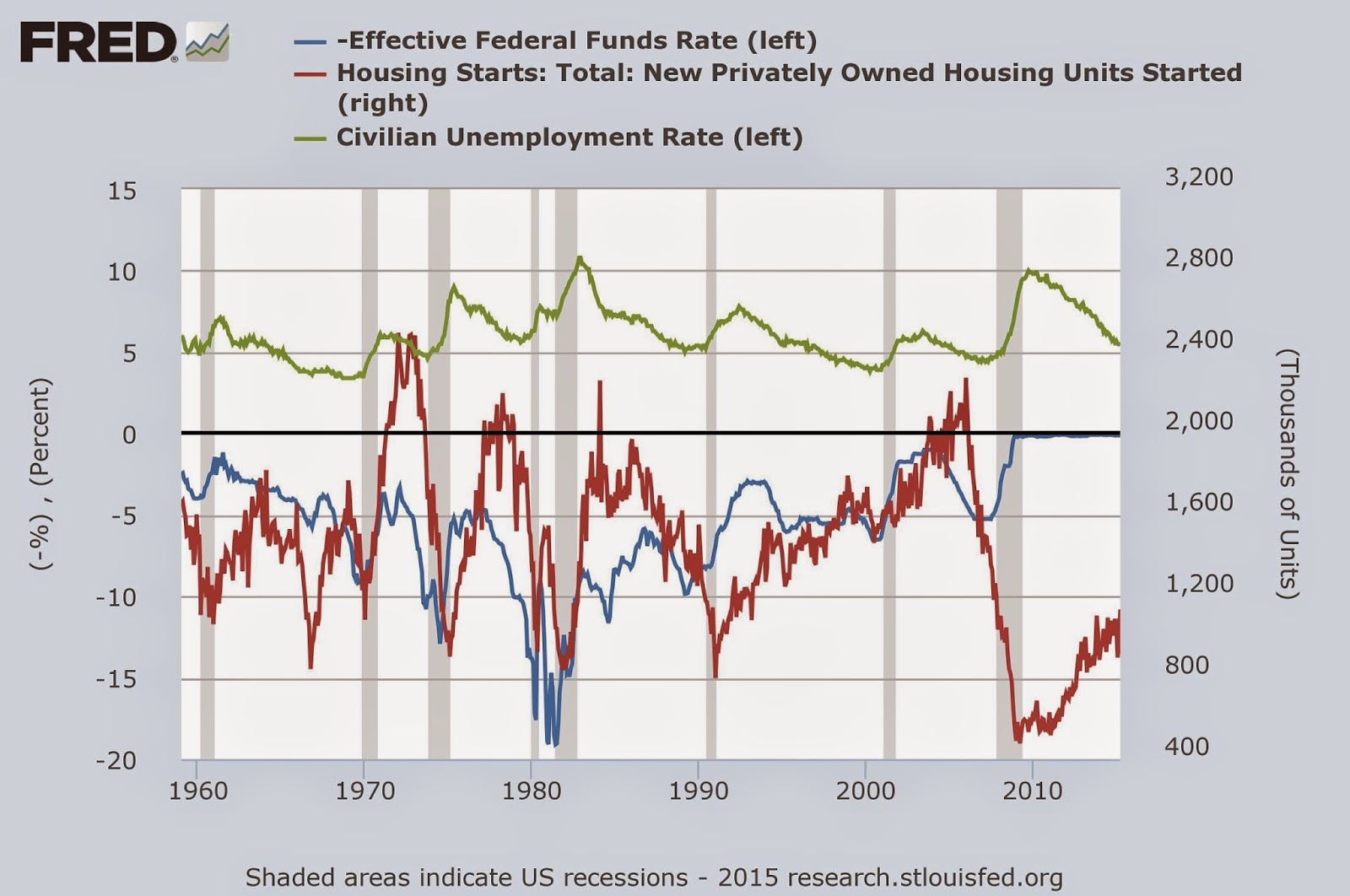

All things being equal, having a college degree is better than not having one. Degree holders make more money and have an easier time finding a job compared to non-degree holders. The difference between just a high school degree and a college degree is over $400 a week (about $20,000/year!). And it's an asset that needs no maintenance and can never be taken away from you. With such large benefits, why shouldn't college be free?

(Of course it's not "free." People on both sides of this argument know it's not "free." But "subsidized so much that the price consumers pay is at or near zero" is too damn long. So I'm calling it "free" for short.)

Free college is not smart policy. For one, it's not entirely clear college debt is a problem. Average debt may be high, but it's driven largely by graduate students. Median balance is just $8,500. And that's only the people who have any debt at all. (To say nothing of subsidization causing the higher tuition in the first place.) Free college is a solution looking for a problem.

But even if this wasn't true, those large internalized benefits make the argument for free college so hard: why shouldn't you pay for something you benefit so much from? Why should other people be forced to shoulder the cost of something that benefits just you? Any externalized benefits to college degrees (slightly lower rates of crimes, for example) are tiny compared to the internalized benefits. With a tertiary enrollment rate of about 90%, any additional incentive would be wasteful. Clearly, further subsidization isn't necessary to encourage people to go to college. If anything, the U.S.'s attendance rate it too high already.

If the benefits are internalized, the costs should be as well. College is the first time in most people's lives where they get to truly customize their education. This isn't merely choosing this or that AP class. This is choosing the most defining aspect of your degree: your major. It determines not only a large share of what classes you'll take, but also the skills you develop and what it says about you as a person. It's no wonder that salaries vary widely by major.

That customization derails another common pro-free college argument: people pay for their own education through the tax system. Higher income means more taxes owed, especially with progressive taxes. It's sort of like a loan. But this is an incredibly sloppy loan system, with cost nonsensically removed from payment.

(Of course it's not "free." People on both sides of this argument know it's not "free." But "subsidized so much that the price consumers pay is at or near zero" is too damn long. So I'm calling it "free" for short.)

Free college is not smart policy. For one, it's not entirely clear college debt is a problem. Average debt may be high, but it's driven largely by graduate students. Median balance is just $8,500. And that's only the people who have any debt at all. (To say nothing of subsidization causing the higher tuition in the first place.) Free college is a solution looking for a problem.

But even if this wasn't true, those large internalized benefits make the argument for free college so hard: why shouldn't you pay for something you benefit so much from? Why should other people be forced to shoulder the cost of something that benefits just you? Any externalized benefits to college degrees (slightly lower rates of crimes, for example) are tiny compared to the internalized benefits. With a tertiary enrollment rate of about 90%, any additional incentive would be wasteful. Clearly, further subsidization isn't necessary to encourage people to go to college. If anything, the U.S.'s attendance rate it too high already.

If the benefits are internalized, the costs should be as well. College is the first time in most people's lives where they get to truly customize their education. This isn't merely choosing this or that AP class. This is choosing the most defining aspect of your degree: your major. It determines not only a large share of what classes you'll take, but also the skills you develop and what it says about you as a person. It's no wonder that salaries vary widely by major.

That customization derails another common pro-free college argument: people pay for their own education through the tax system. Higher income means more taxes owed, especially with progressive taxes. It's sort of like a loan. But this is an incredibly sloppy loan system, with cost nonsensically removed from payment.

Many forms of compensation are not taxable. Jobs differ with varying levels of fulfillment, work hours, flexibility, stress, prestige, and so on. Desirable jobs will have many applicants and undesirable jobs will have few. Differences in wages compensate for differences in working conditions and the fun jobs get a modest paycheck. Yet those favorable conditions cannot be taxed (how would one possibly tax the joy of being a musician?). Some simply won't pay for their education through the tax system. They will learn while others work.

College graduates don't have to be starving artists for this play out. You can live a good life and force strangers to pay for your education without having to pay for the education of strangers. It takes a lot of money in the U.S. to enter the realm of net-tax payer. Only the wealthiest Americans pay any net tax at all. Maybe there's a tax plan out there that will ensure proper payment (and that's a big maybe), but it's unlikely to be fairer than simply paying tuition.

There are already many paths in place to address the big advantage of free college: educational mobility. Increase funding for Pell grants and other programs which target low-income students. There will be more schools like Berea College which charges zero tuition and focuses enrollment on the financially strained. Payments could only be due starting the first few years after college, when incomes are lowest and most in flux. Improve secondary education and encourage trade schools so fewer students drop out (dropouts are most likely to default). We are awash in better solutions.

Not only are these alternatives less costly and more just than free college, they're also far smarter.